By David Fearnley

The volatility that gripped equity markets earlier this week re-emerged overnight, as the US Dow Jones fell more than 1,000 points (3.5%) over concerns that rising interest rates will drag down economic growth. While we don't know when the equity market's recent volatility will settle down, it's important to consider the big picture and not get caught up in short-term changes in sentiment.

Many investors may be looking for reassurance when markets get rocky so we have provided a list of Five Things You Need to Know to Ride Out a Volatile Stock Market.

1. WATCHING FROM THE SIDELINES MAY COST YOU

When markets become volatile, a lot of people try to guess when stocks will bottom out. In the meantime, they often park their investments in cash. But just as many investors are slow to recognise a retreating stock market, many also fail to see an upward trend in the market until after they have missed opportunities for gains.

Missing out on these opportunities can take a big bite out of your returns. Consider that in the 12 months following the end of a bear market, a fully invested stock portfolio had an average total return of 37.4%. However, if an investor missed the first six months of the recovery by holding cash, their return would have been

only 7.5%.

The table below is a hypothetical illustration showing the risk of trying to time the market. By missing just a few of the stock market’s best single-day advances, you could put a real crimp in your potential returns.

2. DOLLAR-COST AVERAGING MAKES IT EASIER TO COPE WITH VOLATILITY

Most people are quick to agree that volatile markets may present buying opportunities for investors with a long-term horizon. But mustering the discipline to make purchases during a volatile market can be difficult. You can’t help wondering, “Is this really the right time to buy?” Dollar-cost averaging can help reduce anxiety about the investment process.

Simply put, dollar-cost averaging is committing a fixed amount of money at regular intervals to an investment. You buy more shares when prices are low and fewer shares when prices are high, and over time, your average cost per share may be less than the average price per share.

Dollar-cost averaging involves a continuous, disciplined investment in fund shares, regardless of fluctuating price levels. Investors should consider their financial ability to continue purchases through periods of low price levels or changing economic conditions.

Such a plan does not guarantee a profit or eliminate risk, nor does it protect against loss in a declining market.

3. NOW MAY BE A GREAT TIME FOR A PORTFOLIO CHECKUP

Is your portfolio as diversified as you think it is?

Meet with your financial adviser to find out. Your portfolio’s weightings in different asset classes may shift over time as one investment performs better or worse than another.

Together with your adviser, you can re-examine your portfolio to see if you are properly diversified. You can also determine whether your current portfolio mix is still a suitable match with your goals and risk tolerance.

4. TUNE OUT THE NOISE AND GAIN A LONGER-TERM PERSPECTIVE

Numerous television stations, websites and social media channels are dedicated to reporting investment news 24 hours a day, seven days a week.

What’s more, there are almost too many financial publications to count. While the media provides a valuable service, they typically offer a very short-term outlook.

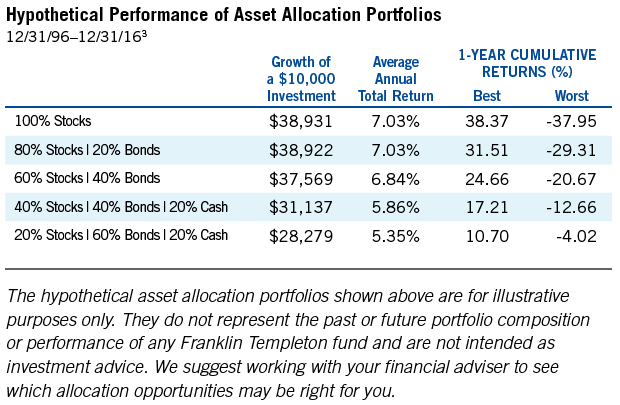

To put your own investment plan in a longer-term perspective and bolster your confidence, you may want to look at how different types of portfolios have performed over time.